- Search

- Riyadh26 ° C

How Better Money Management Can Help You Achieve Your Saving Goals

Lack of proper money management is a key reason why many people in the UAE find it hard to save towards their goals.

Despite the fact that UAE residents do not pay personal income tax, many of them still do not have enough savings.

Experts interviewed by the Khaleej Times identified various causes of this situation: overspending to impress people, lack of a working budget, lack of financial literacy, easy access to credit, and too much spending on non-essential items.

Consequently, if UAE residents want to accomplish their financial goals, they must know how to better manage their money.

In this article, we will identify four things that you can do to improve your money management skills in preparation for a better financial future.

Budgeting

"A budget is telling your money where to go instead of wondering where it went," said John Maxwell, a renowned motivational speaker.

Successful money management must begin with creating a budget and ensuring that every dirham you earn is being planned for.

Without a budget, impulse buying will prevail and after many years of working, you will end up wondering where all the money went.

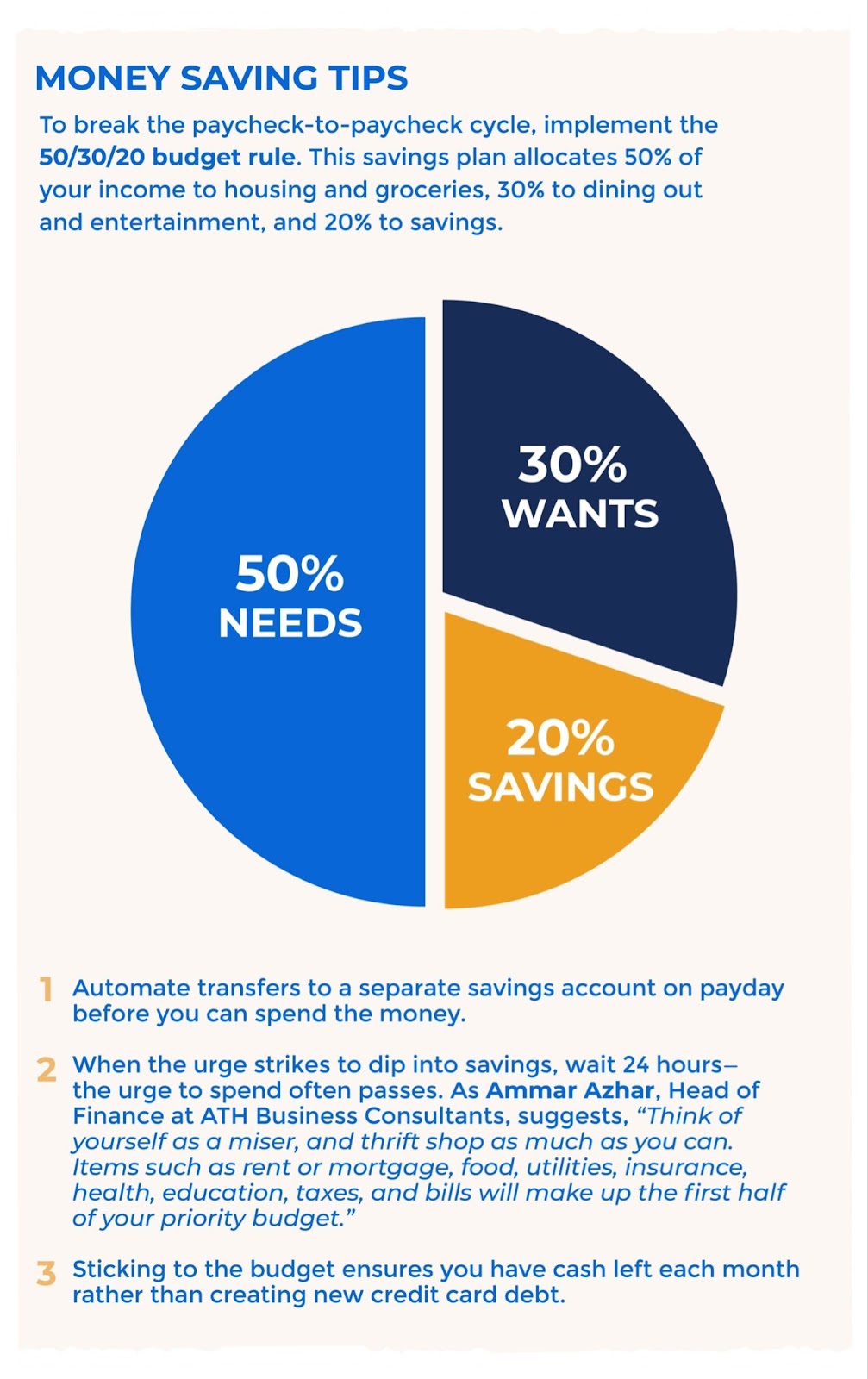

A popular budgeting system that is easy to implement is the 50/30/20 rule. This requires that you budget 50% of your income on your needs (rent, clothing, food, utility bill, etc.), 30% on wants (entertainment, travel, etc.), and save the remaining 20%.

You can go one step further by identifying all the main categories under needs and wants and then allocating specific amounts to them.

Following this rule might mean that you will need to eliminate some items you were spending money on (subscription to an entertainment app, for example) while cutting down spending on some (eating out only once in two weeks instead of every 3 days, for example).

Saving before spending

Saving 20% of your income is a great goal but you might often find yourself in a situation where you are tempted to spend what you should have saved.

One money management tip for avoiding this situation is to save first before spending. You can do this with a money management app like Maly, which allows you to set up automatic deductions from your account.

So, instead of trying to discipline yourself not to spend money you should be saving, you can just set the app up to deduct 20% of your income on every payday.

Keeping track of your spending

Now that you are automatically saving 20% of your income, the next step is to keep track of your finances so that you are not spending too much on one category of expenses to the detriment of another.

You can do this manually by writing your budget for every expense category on a paper or in an excel file and then deducting every new expense in that category.

For example, suppose your budget for eating out is AED 200 for a month. If you visit the restaurant on the 10th, you will deduct the amount spent from AED 200 so you will know how much you have left to spend on eating out for the rest of the month.

A better approach is to use a tool provided by Maly: multiple debit cards.

This allows you to create a debit card for each of your main expense categories, load that card at the beginning of the month with the budgeted amount for the category, then set a spending limit equal to that amount.

You can then monitor your spending on each card from your account dashboard. The advantage of having separate cards is that you can’t make the mistake of overspending on one category (say clothing) to the detriment of another (say food). This “forces” you to be more prudent and to avoid spending unnecessarily.

Setting savings goals

Now that you are saving 20% of your income, you need to set various savings goals (emergency fund, retirement, luxury purchases, downpayment for a property, etc.) and then allocate your savings among them.

Maly also helps with this in two ways. One, you can use its savings goal calculator to calculate how much you will need to be saving every month to meet a particular financial goal.

Second, you can create multiple savings cards for each of your financial goals. This will help you to know how much you have contributed to each goal and how far you have to go to meet it.

Conclusion

Saving money in the UAE is hard, but by improving your money management skills with these four strategies, you can separate yourself from the crowd and start making positive strides towards the financial future you deserve.

And when it seems that following any of these steps is difficult, think about how the joy of the financial future before you (a life of financial freedom and wealth) can transcend any present difficulties.